Die politische Entwicklung Russlands

Seite 1.510 von 4.502vorherige 1 ... 1.4101.4601.5001.5081.5091.5101.5111.5121.5201.5601.610 ... 4.502 nächste

Direkt zur Seite:

Die politische Entwicklung Russlands

17.05.2015 um 19:39Die politische Entwicklung Russlands

17.05.2015 um 19:40@Chavez

ist ja auch okay, fand es trotzdem spanend daran zu erinnern, jeder kann sich doch noch an den stub net virus erinnern, der die Zentrifugen des iranischen Atomprogramms langsam und unbemerkt zerstörte.

ist ja auch okay, fand es trotzdem spanend daran zu erinnern, jeder kann sich doch noch an den stub net virus erinnern, der die Zentrifugen des iranischen Atomprogramms langsam und unbemerkt zerstörte.

Die politische Entwicklung Russlands

17.05.2015 um 19:41Die politische Entwicklung Russlands

17.05.2015 um 19:47@Chavez

na ja , der hat sich nur dran gehangen, die echte Analysen haben andere durchgeführt, superspannendes Thema wie man da vorgegangen ist, und verdammt clever ....aber bisschen ot

na ja , der hat sich nur dran gehangen, die echte Analysen haben andere durchgeführt, superspannendes Thema wie man da vorgegangen ist, und verdammt clever ....aber bisschen ot

Die politische Entwicklung Russlands

17.05.2015 um 19:53@Chavez

Beweise? Nein, es gibt Hinweise dafür, dass Dugins Ideen Putin beeinflussen...hatte nicht Dugin in einer TV-Diskussion am 16.03.14 schon gefordert die Sepas zu bewaffnen und falls dies nicht ausreicht solle die Armee rollen...?

Auch die eurasische Idee ist ja von Dugin bereits in den 90er Jahren propagiert worden, sozusagen als neo-Eurasismus.

Beweise? Nein, es gibt Hinweise dafür, dass Dugins Ideen Putin beeinflussen...hatte nicht Dugin in einer TV-Diskussion am 16.03.14 schon gefordert die Sepas zu bewaffnen und falls dies nicht ausreicht solle die Armee rollen...?

Igor Ryvkinhttps://www.facebook.com/igor.riffking/posts/604988592924564

16. März 2014 ·

Gerade im russischen TV:

Alexander Dugin plädiert für die Bewaffnung Pro Russischer Kräfte in der Ukraine. Wenn das nicht ausreicht, soll offen die Armee rollen. Es soll mindestens der Osten der Ukraine abgespalten werden. Alexander Dugin ist der kulturelle, philosophische und geopolitische Kopf der Politik Russlands.

Chef der liberal-demokratischen Partei Russlands, Wladimir Wolfowitsch Schirinowski: "Ohne russisches Blut können wir die Ukraine nicht erobern. Wir brauchen russisches Blut"

Auch die eurasische Idee ist ja von Dugin bereits in den 90er Jahren propagiert worden, sozusagen als neo-Eurasismus.

Die politische Entwicklung Russlands

17.05.2015 um 20:49@canales

also ich diskutiere hier jetzt ganz bestimmt nicht die Behauptung von einem Niemand bei Facebook und wenn du damit jetzt argumentieren willst lässt das Sehr weit Blicken, hier bist du falsch, öffne ein Thema dort

Verschwörungstheorien

also ich diskutiere hier jetzt ganz bestimmt nicht die Behauptung von einem Niemand bei Facebook und wenn du damit jetzt argumentieren willst lässt das Sehr weit Blicken, hier bist du falsch, öffne ein Thema dort

Verschwörungstheorien

Die politische Entwicklung Russlands

17.05.2015 um 20:54Und? die Idee mit der Eurasischen Union gehört auch nicht Putin, sondern Nasarbajew.canales schrieb:Auch die eurasische Idee ist ja von Dugin bereits in den 90er Jahren propagiert worden, sozusagen als neo-Eurasismus.

Die politische Entwicklung Russlands

17.05.2015 um 21:37Russland war schon immer das Buland...bzw. seit Josef Stalin ist das spätestens so.

Der war halt nicht sonderlich beliebt im Westen - und vor allem bei den Nazis nicht.

Der war halt nicht sonderlich beliebt im Westen - und vor allem bei den Nazis nicht.

Die politische Entwicklung Russlands

17.05.2015 um 21:43das war schon vorher so schau dir die Karikaturen aus der Zarenzeit an.

Der war halt nicht sonderlich beliebt im Westen - und vor allem bei den Nazis nicht.

Die politische Entwicklung Russlands

17.05.2015 um 23:22Die politische Entwicklung Russlands

17.05.2015 um 23:24Die politische Entwicklung Russlands

17.05.2015 um 23:26Die politische Entwicklung Russlands

18.05.2015 um 10:33Forbes: Russland Sanktionen könnten Russland stärken anstatt zu schaden.

Here's How Western Sanctions Have 'Killed' RussiaFortsetzung: http://www.forbes.com/sites/kenrapoza/2015/05/15/heres-how-western-sanctions-have-killed-russia/

McDonald's MCD +0.34% left Crimea. General Motors GM +0.75% left St. Petersburg. Russia is now a pariah state.

The resulting mess?

A 41.5% rise in the Market Vectors Russia (RSX) exchange traded fund, the best emerging market performer this year. And a 17% gain in the ruble year-to-date. It is now trading in the high 40s against the dollar.

Last week, Russia’s biggest food retailer, Magnit , said its retail sales rose by 28.73% in April and added 163 new stores.

According to JPMorgan’s view, however, the Russian government’s financial situation is “quite healthy” thanks to low government debt.

Russia’s current budget surplus is expected to rise to $70 billion (5.5% of the GDP) by the end of the year, up from $59 billion (3.2% GDP) last year.

The weakening of the ruble, the increase in interest rates, and the recession are the three main factors putting pressure on Russian banks. But most non-financial corporations like Magnit have managed to cope with the economic downturn on their own, using internal sources of capital for debt repayment due to restricted access to foreign markets.

Yes, Putin haters…Russian GDP contracted 1.9% year-on-year in the first quarter of 2015. It’s still a tough slog. Russia has massive structural problems we’ve all heard of ad naseum. However, the economy is doing better than expected.

Russia recently jumped from 55th to 26th place in The World Economic Forum’s “2015 Human Capital Report”, an index that ranks nations by their human capital endowment, defined as the skills and capacities that reside in people and that are put to productive use. That puts Russia ahead of start-up nation Israel, and far ahead of the rich, but going-nowhere-fast Euro outdoor museum nations of Italy, Greece, Portugal and Spain. Russia also surpasses Brazil in this regard.

Late next month, the European Commission will meet to discuss Russian sanctions. My guess is sectoral sanctions will end this year, though probably not in July.

Die politische Entwicklung Russlands

18.05.2015 um 10:53Kennt ihr den schon? Schreibt ein Bundespolizist per Whatsapp einem anderen:

http://www.ndr.de/nachrichten/niedersachsen/hannover_weser-leinegebiet/Fluechtlinge-in-Polizeizelle-erniedrigt,misshandlung132.html

Edit: Sorry, falscher Thread

http://www.ndr.de/nachrichten/niedersachsen/hannover_weser-leinegebiet/Fluechtlinge-in-Polizeizelle-erniedrigt,misshandlung132.html

"Hab den weggeschlagen. Nen Afghanen. Mit Einreiseverbot. Hab dem meine Finger in die Nase gesteckt. Und gewürgt. War witzig. Und an den Fußfesseln durch die Wache geschliffen. Das war so schön. Gequikt wie ein Schwein. Das war ein Geschenk von Allah", ist dort zu lesen gewesen.Dein Freund und Helfer!

Edit: Sorry, falscher Thread

Die politische Entwicklung Russlands

18.05.2015 um 10:57Oder auch nicht:Ukrop schrieb:Forbes: Russland Sanktionen könnten Russland stärken anstatt zu schaden.

Forbes: A Russian Crisis With No End In Sight, Thanks To Low Oil Prices And Sanctions

Former Russian prime minister Evgeny Primakov warned that, if Vladimir Putin continues his Ukraine policies, Russia will become a pariah third-world petro state. The fundamentals of the Russian economy, as it enters 2015, suggest that Russia is fulfilling Primakov’s prophesy. Russia’s fate depends on economic factors beyond its control (energy prices and gas markets) and on Putin’s continued international adventurism, which he is loath to abandon for fear of regime change. Putin can no longer keep his promise to the Russian people of prosperity and stability. No wonder his propagandists are fighting full time to convince the West to drop its sanctions. Unlike the 2008/9 financial crisis, Russia faces a long and deep recession because the underlying causes are unlikely to go away in the near term.http://www.forbes.com/sites/paulroderickgregory/2015/05/14/a-russian-crisis-with-no-end-in-sight-thanks-to-low-oil-prices-and-sanctions/

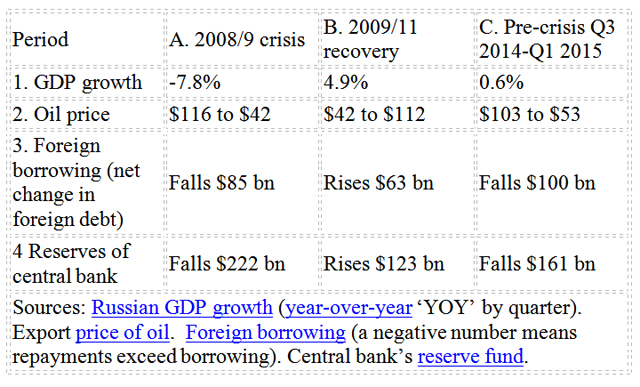

The two crises compared

The Russian economy has been struck by lightning twice during the short span of seven years. In 2008/9, a massive storm of falling oil prices and credit-market collapse struck Russia along with the rest of the world. The storm inflicted more serious damage on Russia than elsewhere (an 8 percent drop in GDP), but it passed over relatively quickly as oil prices recovered and world credit markets unfroze. In the 2010-11 period, economic growth averaged 5 percent, before falling to anemic rates in the buildup to Ukraine. Lightning struck Russia again in mid-2014 with the worldwide collapse of energy prices and Ukraine sanctions that bumped Russia from credit markets.

The initial voltages of the 2008/9 and 2014 lightning strikes were about the same, but the damage will be longer and deeper the second time around. Low energy prices will not disappear soon, and sanctions will remain in place as long as Russia makes no serious moves toward peace in Ukraine.

The accompanying table shows the same negative factors at play during the 2008/9 financial crisis (Column A) and the current “precrisis” period (Column C), with similar collapses of oil prices (Row 2), foreign borrowing (Row 3), and diminishing central bank reserves (Row 4). Column B shows the quick comeback from the 2008/9 crisis, with rising oil prices, revived foreign borrowing, and a restocking of central bank foreign exchange reserves.

From whence is Russia’s second comeback to emerge this time around? Despite divergent opinions on the long run, oil prices are expected to remain low for the foreseeable future. As long as financial sanctions remain in place, Russia has few sources of external borrowing for investing in and refinancing its highly leveraged companies. Russia had little control over the first lightning strike. The world recession drove down energy prices, and Russia lost access to world credit markets as credit froze to emerging markets. If Russia had less dependence on energy and had kept its hands, troops, and equipment out of Crimea and east Ukraine, it could have mitigated the second strike. But it did not.

...

Die politische Entwicklung Russlands

18.05.2015 um 11:07Hehe, danke für den Beleg dafür dass die westliche Presse nur Müll schreibt und sich dauernd selbst widerspricht. Sogar innerhalb der selben Zeitung.Larry08 schrieb:Oder auch nicht:

Forbes: A Russian Crisis With No End In Sight, Thanks To Low Oil Prices And Sanctions

Wie kann man nur in so eine Propagandawelt leben und und wahr von falsch unterscheiden?

Zum Glück sind russische Medien konsistenter.

Die politische Entwicklung Russlands

18.05.2015 um 11:14@Ukrop

Danke, das Du meine Meinung bestätigst. Freie Meinung ist in Russland Scheiße, nichts geht doch über einheitliche Medien, in denen stets die Staatsdorktrin verkündet werden. Feine Sache, das !

Danke, das Du meine Meinung bestätigst. Freie Meinung ist in Russland Scheiße, nichts geht doch über einheitliche Medien, in denen stets die Staatsdorktrin verkündet werden. Feine Sache, das !

Die politische Entwicklung Russlands

18.05.2015 um 11:14@Ukrop

Ja furchtbar, wenn ein Thema aus mehreren Perspektiven beleuchtet und analysiert wird.

Da muss man ja dann drüber nachdenken.

Da ist es schon entspannter, wenn einem ein russisches Staatsmedium erzählt, dass alles dufte ist und Putin als Politiker nie falsche Entscheidungen trifft.^^

Ja furchtbar, wenn ein Thema aus mehreren Perspektiven beleuchtet und analysiert wird.

Da muss man ja dann drüber nachdenken.

Da ist es schon entspannter, wenn einem ein russisches Staatsmedium erzählt, dass alles dufte ist und Putin als Politiker nie falsche Entscheidungen trifft.^^